Ever feel like your credit card balance is a treadmill you can't get off? You pay, and pay, and the number barely budges. That, my friend, is the magic (or misery) of credit card interest at play. It's not some abstract financial concept; it's real money leaving your pocket, often without you even realizing the full extent of it.

I'm here to pull back the curtain. No fancy jargon, no sugar-coating. Just the raw truth about how credit card interest works, why it matters, and how you can stop being a victim and start being the boss of your own money.

What Exactly Is Credit Card Interest?

Think of it like this: when you use your credit card, you're essentially borrowing money from the bank. They're not doing it out of the goodness of their hearts. They charge you a fee for that loan, and that fee is called interest.

It's the cost of convenience, the price of flexibility. And if you're not careful, it can become the most expensive convenience you've ever paid for.

APR: The Big Number You Can't Ignore

When you get a credit card, you'll see a number called the Annual Percentage Rate (APR). This is the yearly rate of interest you'll be charged on your outstanding balance.

But here's the kicker: most people don't pay interest annually. Credit card companies calculate interest daily. So, that APR gets broken down into a Daily Periodic Rate (DPR).

It's a small number, sure, but it adds up faster than you think. Especially when you carry a balance.

The Average Daily Balance Method: How They Calculate Your Pain

This is where it gets a little tricky, but stick with me. Most credit card companies use the average daily balance method to figure out how much interest you owe.

They don't just look at your balance at the end of the month. Oh no. They take your balance each day, add them all up, and then divide by the number of days in the billing cycle. That gives them your average daily balance.

Then, they multiply that average daily balance by your daily periodic rate. Boom. That's your interest charge for the month. It's a subtle system, designed to keep you paying.

Let's break it down with an example. Imagine your billing cycle is 30 days.

•Days 1-10: You have a balance of $1,000.

•Day 11: You make a $200 payment, so your balance drops to $800.

•Days 11-20: Your balance is $800.

•Day 21: You make a $300 purchase, bringing your balance to $1,100.

•Days 21-30: Your balance is $1,100.

Your average daily balance wouldn't be $1,100, or $800, or even $1,000. It would be a weighted average, reflecting every single day's balance. This is why making payments early in the cycle can save you money.

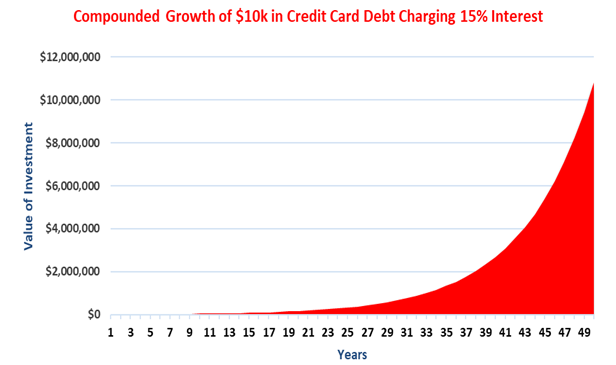

The Silent Killer: Compound Interest on Your Debt

You've heard of compound interest being a superpower for saving, right? Money making money? Well, it's a supervillain when it comes to debt.

Credit card interest compounds. This means you're not just paying interest on the money you borrowed; you're paying interest on the interest you already owed.

It's a vicious cycle. Your balance grows, the interest grows, and suddenly, a small debt becomes a monster. This is how people get trapped.

Take a look at this. This chart shows how quickly debt can snowball when compound interest is involved. It's not pretty.

The Minimum Payment Trap

Credit card companies love minimum payments. Why? Because they keep you in debt longer, which means more interest for them. It's a brilliant business model, if you're the bank.

If you only pay the minimum, you're barely touching the principal. Most of your payment goes straight to interest. It's like trying to empty a swimming pool with a teaspoon while someone else is filling it with a fire hose.

Real Talk: Stories and Examples That Hit Home

I've seen it countless times. A young entrepreneur, full of ambition, uses a credit card to cover initial business expenses. Maybe a few thousand bucks. They think they'll pay it off quickly once the business takes off.

But then, sales are slow. Expenses pile up. And that initial few thousand dollars, with a 20% APR, starts to feel like a lead weight around their neck. Every month, the interest charges eat into their already tight budget.

Example: The $1,000 Purchase That Cost $2,000

Let's say you buy a new laptop for $1,000 on your credit card with a 24% APR. You decide to only make the minimum payment, which is often around 2-3% of your balance, or $25, whichever is higher.

•Month 1: Balance $1,000. Minimum payment $25. Interest charged: ~$20. Principal paid: $5. New balance: $995.

•Month 2: Balance $995. Minimum payment $25. Interest charged: ~$19.90. Principal paid: $5.10. New balance: $989.90.

See the pattern? You're barely making a dent. Over time, that $1,000 laptop could easily cost you double, maybe even triple, once all the interest is factored in. It's a silent killer of wealth.

The

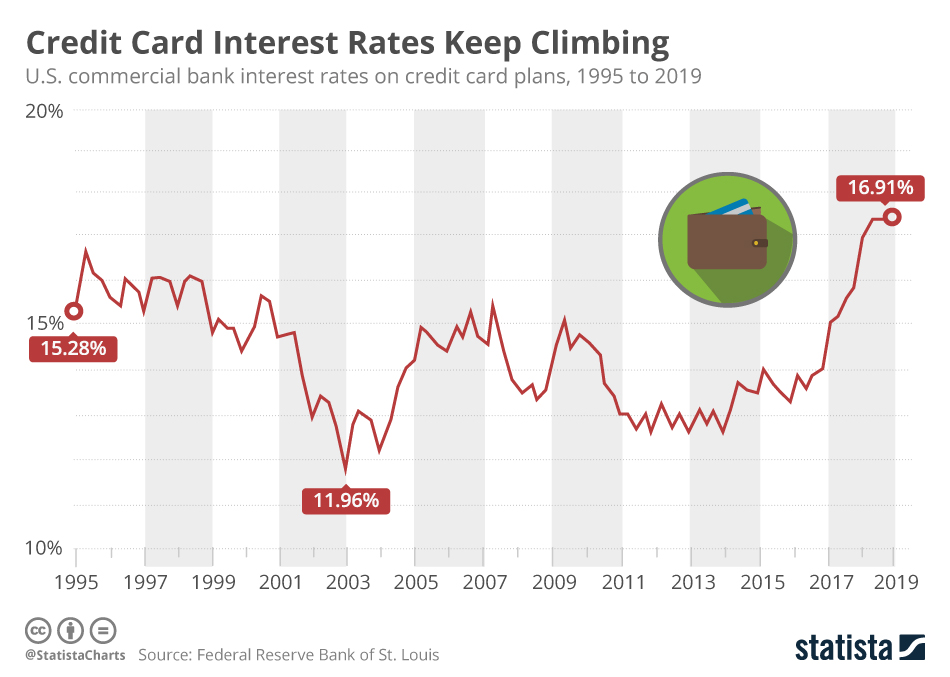

The Highs and Lows of Credit Card Interest Rates

Credit card interest rates aren't static. They fluctuate based on the market, your creditworthiness, and even the type of card you have. Some cards offer introductory 0% APR periods, which can be a great tool if used wisely. Others, especially those for people with lower credit scores, can hit you with APRs north of 25% or even 30%.

This chart shows how credit card interest rates have moved over time. Notice the trends, and how they can impact your financial health.

When rates are high, every dollar you carry in debt costs you more. It's simple math, but it's often overlooked until it's too late.

How to Beat the System: Strategies to Minimize Credit Card Interest

Alright, enough with the doom and gloom. You're here to learn how to win, right? Here's the playbook to stop paying unnecessary credit card interest and start taking control.

1. Pay Your Balance in Full, Every Single Month

This is the golden rule. If you pay your statement balance in full by the due date, you generally won't pay any interest. Credit card companies offer a grace period, usually 21-25 days, between the end of your billing cycle and your payment due date. Use it.

If you can't do this, you're essentially signing up to pay extra for everything you buy. And who wants that?

2. Understand Your Billing Cycle and Due Dates

Knowing when your billing cycle closes and when your payment is due is crucial. Payments made after the billing cycle closes but before the due date still avoid interest on new purchases. But if you carry a balance, those new purchases might start accruing interest immediately.

It's a small detail, but it can save you a lot of cash.

3. Make More Than the Minimum Payment

I can't stress this enough. If paying in full isn't an option, pay as much as you possibly can above the minimum. Even an extra $20 or $50 can drastically reduce the time it takes to pay off your debt and the total interest you'll pay.

Here's why it matters:

•Reduces Principal Faster: More of your payment goes towards the actual debt, not just the interest.

•Less Interest Accrued: A lower principal means less interest calculated on your average daily balance.

•Faster Debt Freedom: You'll get out of debt sooner, freeing up your money for things that actually matter to you.

4. Tackle High-Interest Debt First (The Debt Avalanche)

If you have multiple credit cards, focus your extra payments on the card with the highest APR. This strategy, often called the

4. Tackle High-Interest Debt First (The Debt Avalanche)

If you have multiple credit cards, focus your extra payments on the card with the highest APR. This strategy, often called the debt avalanche, saves you the most money on interest in the long run. You pay the minimum on all other cards, and throw every extra dollar at the one costing you the most.

It’s purely mathematical. It’s about optimizing your cash flow to minimize the bank’s cut.

5. Consider the Debt Snowball (For Psychological Wins)

While the debt avalanche is financially superior, some people prefer the debt snowball method. Here, you focus on paying off the smallest balance first, regardless of the interest rate. The idea is that quick wins provide motivation to keep going.

It’s less about the numbers and more about the momentum. Pick the method that you’ll actually stick with.

6. Balance Transfers: A Temporary Reprieve

Got a high-interest balance? A balance transfer card might offer a 0% APR for an introductory period (e.g., 12-18 months). This can be a lifesaver, giving you time to pay down your principal without interest eating away at your payments.

But here’s the catch: there’s usually a balance transfer fee (around 3-5% of the transferred amount). And if you don’t pay off the balance before the introductory period ends, you’ll be hit with the regular, often high, APR.

It’s a tool, not a magic wand. Use it strategically, with a clear plan to pay off the debt.

7. Negotiate with Your Creditor

Don’t be afraid to call your credit card company. Seriously. If you’re struggling, explain your situation. They might be willing to lower your APR, waive a late fee, or even set up a payment plan. They’d rather get some money than no money.

It’s not guaranteed, but a quick phone call could save you hundreds, even thousands, of dollars. What’s the worst they can say? No?

The Bottom Line: Your Money, Your Power

Credit card interest isn’t some abstract concept. It’s a powerful force that can either work for you (when you earn it on savings) or against you (when you pay it on debt). Understanding how it works is the first step to taking back control.

Don’t let the banks dictate your financial future. Learn the rules, play smart, and keep more of your hard-earned cash in your pocket. Because at the end of the day, your money should be working for you, not against you.

No comments:

Post a Comment