Ever feel like debt is a monster breathing down your neck? You're not alone. Most people wake up every day with that nagging feeling, wondering how they're ever going to get out from under it.

I get it. I've seen countless individuals and businesses paralyzed by debt, stuck in a cycle they can't seem to break. But here's the truth: you can break free, and it doesn't have to be complicated.

Today, we're going to cut through the noise and talk about two powerful strategies to obliterate your debt: the Debt Snowball vs Avalanche methods. We'll figure out which one is your weapon of choice.

The Debt Monster: Why We're Here

Let's be real. Debt isn't just about numbers on a spreadsheet.

It's about stress, lost sleep, and missed opportunities. It's about feeling trapped.

But what if I told you there's a way to turn that feeling of dread into a feeling of absolute control? A way to systematically dismantle your debt, piece by piece, until it's nothing but a bad memory?

That's what these methods offer. They're not magic, they're strategy.

Method 1: The Debt Snowball – Building Momentum

Imagine a small snowball rolling down a hill. It starts tiny, but as it picks up speed, it gathers more snow, growing bigger and bigger.

That's the essence of the Debt Snowball method. It's all about psychological wins, building momentum, and getting you addicted to success.

How the Debt Snowball Works

This method is deceptively simple, and that's its genius. You list all your debts from the smallest balance to the largest, regardless of the interest rate.

Then, you attack the smallest debt with everything you've got, while making minimum payments on all your other debts. Once that smallest debt is gone, you take the money you were paying on it and add it to the payment of the next smallest debt.

It's like a financial domino effect. Each debt you pay off frees up more cash to throw at the next one, creating a powerful snowball of payments.

Here's the breakdown:

1.List your debts: Order them from the smallest outstanding balance to the largest.

2.Minimum payments: Make only the minimum payment on all debts except the smallest one.

3.Attack the smallest: Throw every extra dollar you have at the debt with the smallest balance.

4.Roll it over: Once the smallest debt is paid off, take the money you were paying on it (minimum payment + extra payment) and add it to the minimum payment of the next smallest debt.

Why the Snowball Works (The Psychology of Winning)

This isn't about optimizing interest payments. This is about human behavior.

When you pay off that first small debt, you get a rush. A win. That feeling of accomplishment is incredibly powerful.

It fuels your motivation to keep going, to tackle the next one. It turns a daunting, overwhelming task into a series of achievable victories.

Think about it. If you're staring down $50,000 in debt, paying off a $500 credit card feels like a massive achievement. It's tangible progress.

This psychological boost is often the missing piece for people who struggle with debt repayment. It keeps them in the game.

The Downside (The Math Guy's Grumble)

Okay, so it's not perfect. The math purists will tell you that you'll likely pay more in interest with the Debt Snowball method.

And they're not wrong. By focusing on smaller balances first, you might leave higher-interest debts accruing more interest for longer.

But here's my take: if the psychological win keeps you motivated and consistent, then it's the better method for you. Consistency beats perfection every single time.

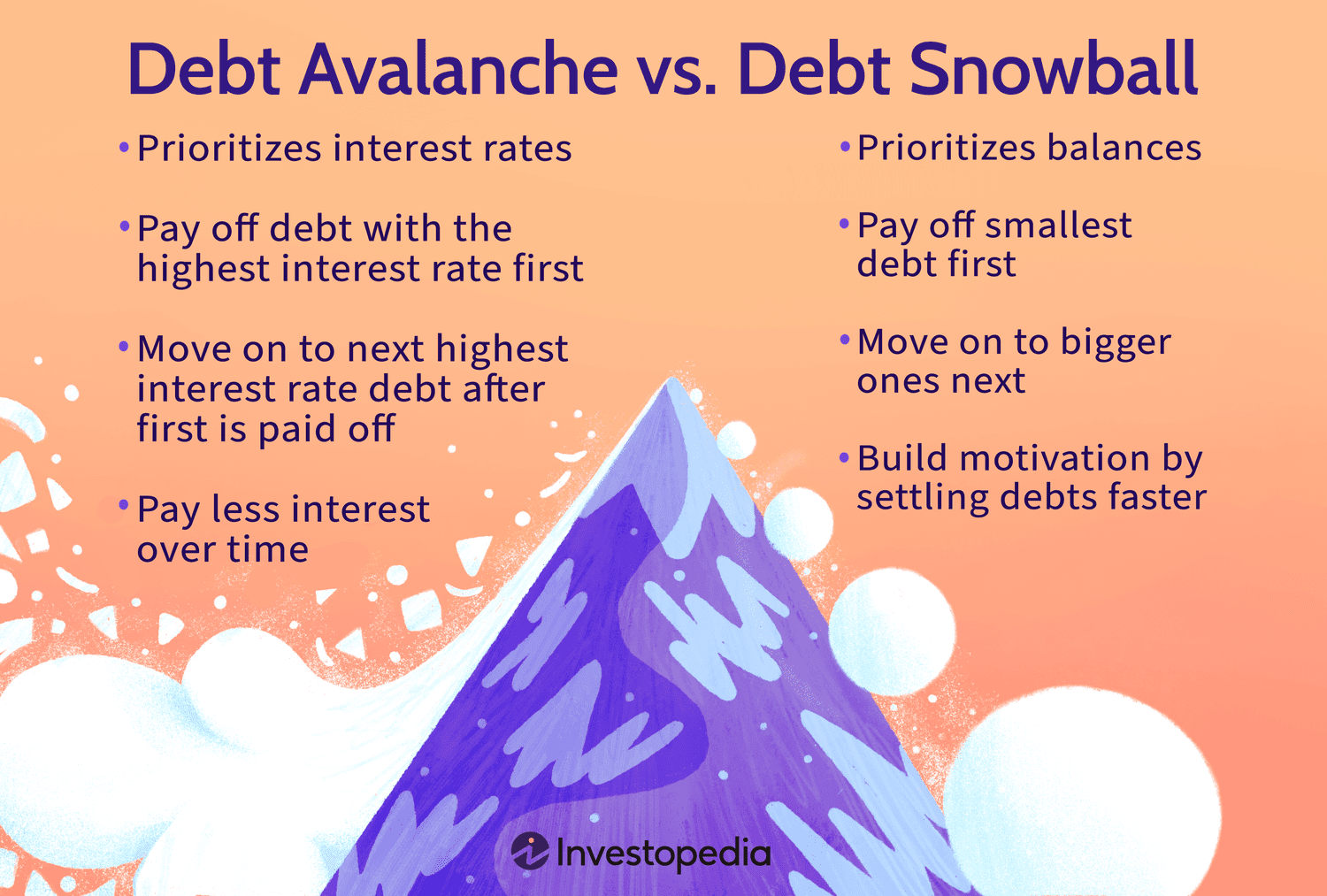

Debt Snowball vs Avalanche: A Quick Comparison

To give you a clearer picture, here's a quick rundown of how these two methods stack up. It's not about one being inherently 'better' than the other, but about which one aligns with your psychology and your financial situation.

Feature | Debt Snowball | Debt Avalanche |

Primary Focus | Psychological wins, motivation, quick victories | Financial efficiency, saving on interest |

Debt Order | Smallest balance to largest | Highest interest rate to lowest |

Initial Progress | Faster, more frequent small wins | Slower, especially with large high-interest debts |

Interest Paid | Potentially more interest paid overall | Least amount of interest paid overall |

Motivation Style | Builds momentum through achievement | Relies on discipline and long-term financial gain |

Now, let's talk about the Debt Avalanche. This is the method the math nerds love, and for good reason.

It's cold, calculated, and designed to save you the most money in interest. No warm fuzzy feelings here, just pure financial efficiency.

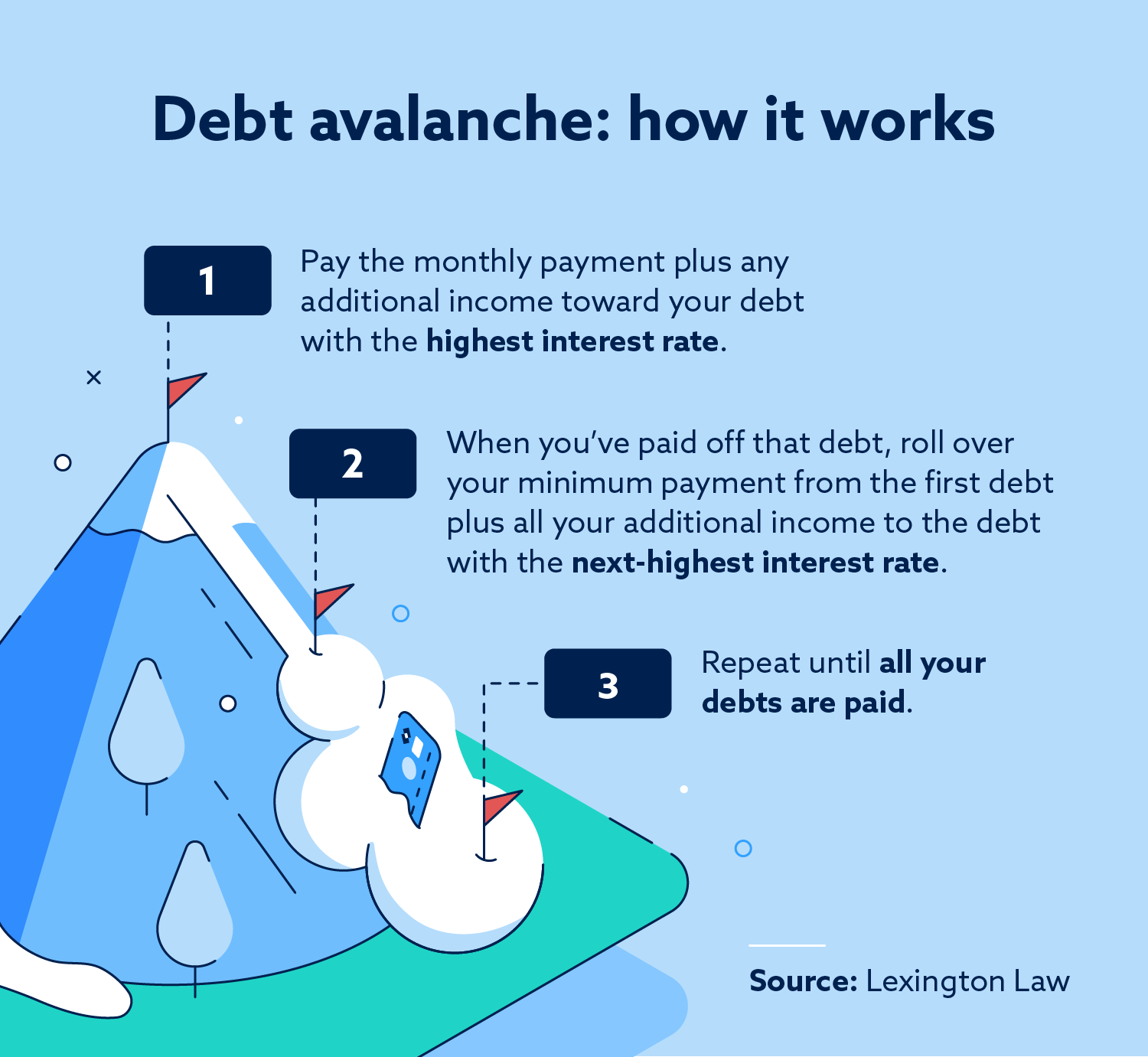

How the Debt Avalanche Works

With the Debt Avalanche, you're going after the most expensive debt first. You list all your debts from the highest interest rate to the lowest.

You then throw every extra dollar you have at the debt with the highest interest rate, while making minimum payments on all your other debts. Once that high-interest debt is gone, you take that payment and roll it into the next highest interest rate debt.

It's like triggering an avalanche. You hit the biggest, most impactful problem first, and the momentum builds as you eliminate each one.

Here's how to execute it:

1.List your debts: Order them by interest rate, from highest to lowest.

2.Minimum payments: Make only the minimum payment on all debts except the one with the highest interest rate.

3.Attack the highest: Direct every extra dollar you have at the debt with the highest interest rate.

4.Roll it over: Once that debt is paid off, take the money you were paying on it (minimum payment + extra payment) and add it to the minimum payment of the next highest interest rate debt.

5.Repeat: Continue this process until all your debts are eliminated.

Why the Avalanche Works (The Mathematical Advantage)

This method is all about saving you money. By targeting the debts that are costing you the most in interest, you reduce the total amount you pay over the life of your loans.

It's financially optimal. If you have a significant amount of high-interest debt, like credit card balances, the Avalanche method can save you thousands of dollars and shave years off your repayment time.

It's a logical, no-nonsense approach for those who can stick to it, even without the immediate gratification of small wins.

The Downside (The Motivation Hurdle)

The biggest challenge with the Debt Avalanche is psychological. If your highest interest rate debt also happens to be your largest balance, it can feel like you're not making much progress for a long time.

Those early wins, which are so crucial for motivation in the Snowball method, are often absent here. You might be chipping away at a massive debt for months, even years, before you see it disappear.

This can lead to burnout and a loss of motivation, which ultimately can derail your entire debt repayment plan. Remember, the best plan is the one you actually stick to.

Debt Snowball vs Avalanche: Which One Should YOU Choose?

This is the million-dollar question, right? And like most things in life, there's no one-size-fits-all answer. It comes down to understanding yourself and your financial situation.

When to Use the Debt Snowball

•You need quick wins: If you're easily discouraged or need to see tangible progress to stay motivated, the Snowball method is your champion. Those small victories will keep you in the fight.

•You have many small debts: If you're juggling a bunch of small credit card balances or personal loans, knocking them out quickly can provide immense psychological relief and simplify your financial life.

•You've tried other methods and failed: If you've attempted to pay down debt before and lost steam, the Snowball's motivational aspect might be exactly what you need to finally succeed.

When to Use the Debt Avalanche

•You're a numbers person: If you're disciplined, motivated by saving money, and can stick to a plan even without immediate gratification, the Avalanche method will save you the most cash.

•You have high-interest debt: If a significant portion of your debt is carrying sky-high interest rates (think credit cards with 20%+ APR), the Avalanche method will minimize the financial bleed.

•You have fewer debts: If you have a handful of larger debts, the Avalanche can be a straightforward way to tackle them efficiently.

My Take: It's About Behavior, Not Just Math

Look, the math is clear: the Debt Avalanche saves you more money. Period. But personal finance isn't just math; it's personal.

It's about your habits, your discipline, and your ability to stay consistent. If the mathematically superior method makes you quit after three months because you're not seeing progress, then it's not superior for you.

I've seen people get rich doing things that aren'tmathematically optimal, simply because they stuck with it. Consistency is the ultimate leverage.

So, ask yourself:

•Am I the kind of person who needs quick wins to stay motivated?

•Or am I disciplined enough to play the long game for maximum financial gain?

Be honest with yourself. Your answer will tell you which method is right.

Real Talk: Beyond Snowballs and Avalanches

Choosing between the Debt Snowball vs Avalanche is a great first step. But let's be clear: these are just tools. They won't work if you don't address the root causes of your debt.

Here are some hard truths and actionable steps to supercharge your debt repayment journey, no matter which method you choose:

1. Stop the Bleeding First

Before you even think about paying down debt, you have to stop accumulating new debt. This sounds obvious, but most people skip this step.

•Cut up credit cards: If you can't control your spending, get rid of the temptation. Seriously.

•Create a brutal budget: Know exactly where every dollar goes. Every. Single. Dollar. If you don't track it, you can't control it.

•Identify spending triggers: What makes you spend unnecessarily? Is it stress? Boredom? Social pressure? Figure it out and build defenses.

2. Increase Your Income (The Ultimate Cheat Code)

Paying off debt faster isn't just about cutting expenses. It's about increasing the firepower you have to throw at it.

•Side hustles: Deliver food, walk dogs, freelance your skills. There are a million ways to make an extra few hundred bucks a month. Stop making excuses.

•Negotiate a raise: If you're valuable, ask for what you're worth. The worst they can say is no.

•Sell your junk: You probably have thousands of dollars sitting around your house in unused items. Sell it. Convert clutter into cash.

3. Build an Emergency Fund (Your Debt Shield)

This is non-negotiable. Life happens. Car breaks down. Medical emergency. If you don't have cash set aside, you'll be right back in debt when disaster strikes.

•Start small: Aim for $1,000 first. Just get it done.

•Grow it: Once your debt is gone, build it up to 3-6 months of living expenses. This is your financial fortress.

4. Stay Consistent, Stay Focused

This isn't a sprint; it's a marathon. There will be days you want to quit. Days you feel like you're not making progress.

•Track your progress: Seeing those balances drop is a huge motivator. Use a spreadsheet, an app, or even a whiteboard.

•Celebrate small wins: When you pay off a debt, acknowledge it. You earned that victory.

•Find an accountability partner: Someone who will kick you in the butt when you need it and celebrate with you when you succeed.

The Bottom Line: Your Debt-Free Future

Whether you choose the Debt Snowball vs Avalanche method, the most important thing is to choose one and stick with it. Don't overthink it. Don't get paralyzed by analysis.

Start today. Make a plan. Execute relentlessly. Your future self, free from the chains of debt, will thank you. The path to financial freedom begins with a single, decisive step. Now go take it.

No comments:

Post a Comment