How much debt is too much?

It’s the question that keeps you staring at the ceiling at 3 AM.You’re wondering if that car payment is a ladder or a shovel.Most people are just digging a hole and calling it "living the dream."

I get it because I’ve been there, looking at a bank account that didn't match my ambitions.The world tells you to buy things you don't need with money you don't have.Then you end up working a job you hate to pay for a life you don't even like.

We aren't doing the formal, academic BS today.This is real talk about your freedom and your math.If the math doesn't work, you don't work—you just survive.

The Math of "How Much Debt is Too Much?"

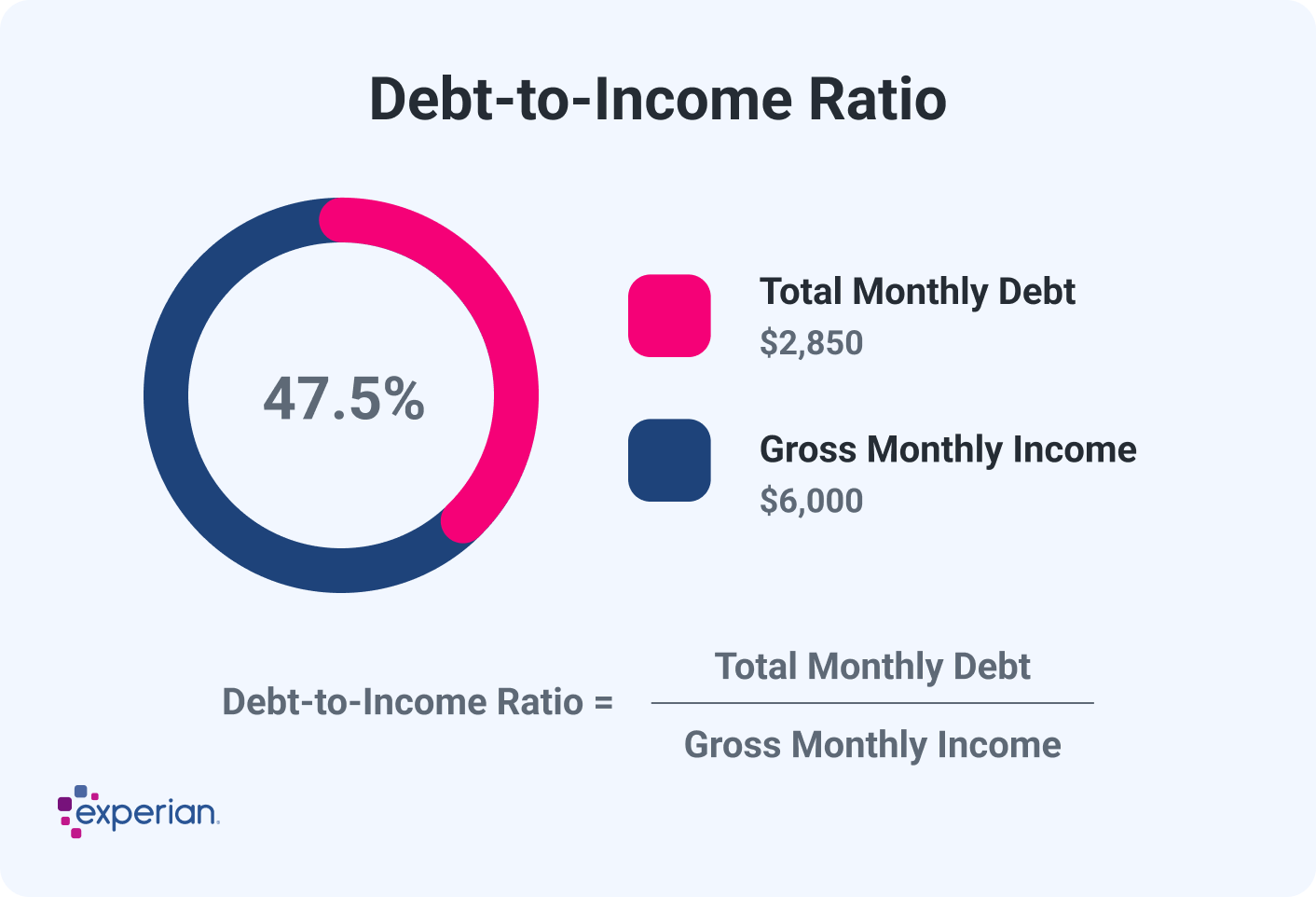

Forget what your neighbor is driving or what the bank says you "qualify" for.Banks want you in debt because that’s how they make their billions.Your personal health is measured by one number: your Debt-to-Income (DTI) ratio.

Think of it as the speed at which you’re bleeding cash every month.It’s the percentage of your gross income that goes straight to someone else’s pocket.The higher that number, the less you own your own life.

Here is how you actually calculate it without a PhD:

•Step 1: Add up every single monthly debt payment (rent, car, cards, student loans).

•Step 2: Find your gross monthly income (the big number before taxes steal half).

•Step 3: Divide the debt by the income and multiply by 100.

If you pay $3,000 in debt and make $6,000, your DTI is 50% .That means you work two weeks every month just to stay at zero.That is a lot of life to trade for a "good" credit score.

The Benchmarks: When Are You Redlining?

Lenders have their own "safe" zones, but they aren't your friends.They want you just enough in debt that you keep paying, but not so much that you go bust.Here is the reality of the percentages you’re looking at:

•36% or less: This is the "safe" zone where you can actually build wealth .

•37% to 43%: You are officially "stretched" and one bad week away from a crisis .

•44% or more: You are redlining, and the engine is about to blow .

If more than 40% of your check is gone before you buy a single taco, you’re in trouble.You have no margin for error, no room for investment, and no peace.You aren't building an empire; you're building a prison.

Good Debt vs. Bad Debt: The Leverage Lie

People love to talk about "good debt" like it’s a magic pill.They say a mortgage is an asset, but an asset puts money in your pocket.A house takes money out of your pocket every single month.

The Reality of Good Debt

Good debt is leverage used to buy something that pays you back more than it costs.If you borrow at 5% to make 15%, you’re a genius.If you borrow at 5% to buy a depreciating hunk of metal, you’re a customer.

•Real Estate: Can be good if the rent covers the debt and then some .

•Education: Only good if the ROI on the salary jump is massive .

•Business: The best leverage if you actually know how to run a business.

The Poison of Bad Debt

Bad debt is just consumption with a "pay later" sticker that never falls off.It’s buying a lifestyle you haven't earned yet.It’s the ultimate tax on people who can’t wait.

•Credit Cards: 20%+ interest is a financial death sentence.

•New Cars: You lose 20% of the value the second you drive off the lot.

•Payday Loans: These are just legal ways to rob people in broad daylight.

If it doesn't make you money, it’s probably bad debt.

Stop calling your liabilities "investments" just to feel better about the payment.Call it what it is: a cost.

5 Signs You Have Too Much Debt Right Now

Sometimes the numbers lie because you’re "managing" the payments.But "managing" is just a fancy word for "barely hanging on."If any of these sound like you, the alarm is already going off:

1.The Minimum Payment Trap: You only pay the minimum on your cards .

2.The Bill Shuffle: You pay the electric bill late so you can pay the car on time .

3.The Ostrich Method: You stop opening the envelopes because they stress you out .

4.Credit for Calories: You’re putting groceries on a credit card because the cash is gone.

5.Zero Margin: You have no emergency fund because the debt ate it all.

Money stress is the #1 killer of relationships and sleep.If you’re fighting about the "how much debt is too much" question, you already know the answer.You have too much.

The Playbook: How to Kill the Debt

You don't need a complex 12-step program or a life coach.You need to stop spending money you don't have and start making more.Here is the Hormozi-approved way to get your life back:

Step 1: Face the Ugly Truth

Get a piece of paper and write down every single cent you owe.Don't round down, don't forget the "small" stuff.Look at the total number until it makes you sick enough to change.

Step 2: Stop the Bleeding

You cannot fill a bucket that has a hole in the bottom.Cut the cards, cancel the subscriptions, and stop going out.If you’re in a hole, the first rule is to stop digging.

Step 3: Choose Your Weapon

Pick a strategy and stick to it for longer than a week.The Snowball Method is for the psychological win—kill the small debts first.The Avalanche Method is for the math win—kill the high interest first.

I prefer the Snowball because momentum is the only thing that keeps people going.Once that first $500 card is gone, you feel like a winner.Winners keep winning.

Step 4: Sell Your Crap and Work More

If you have a $50,000 truck and $50,000 in debt, sell the truck.Drive a $5,000 beater until you’re rich enough to not care.Then, go get a second job or start a side hustle.

Every extra dollar you make should go straight into the debt fire.Don't buy a "reward" for paying off a card.The reward is the freedom you’re buying back.

The Bottom Line: Freedom is the Goal

Most people spend their whole lives as slaves to a monthly payment.They trade 40 hours a week for a car they don't drive and a house they aren't in.That is a bad trade.

You want to get to a place where you own your time.You can't own your time if the bank owns your paycheck.It takes discipline, it takes sacrifice, and it takes being "weird" compared to your friends.

But being "weird" is better than being broke and stressed.Decide today that you’re done being a customer for the banks.Start the math, kill the debt, and get your life back.

Maybe you are interested in this: How to find multi bagger stocks early?

No comments:

Post a Comment